A History of Financial Aid & Student Debt

Tuition-Free to Debt Based Economy: A History of Financial Aid & the Rise of Corporations

The modern U.S. economy relies heavily on credit and borrowing. Households use mortgages to purchase homes, auto loans to buy vehicles, and credit cards to manage short-term expenses. Student loans have become another major component of this broader credit-based system.

Higher education has evolved alongside this shift. Colleges and universities that were once primarily supported by public funding and philanthropic contributions now depend significantly on tuition revenue, endowment management, bond financing, and auxiliary enterprises. Many institutions operate with financial structures similar to large nonprofit corporations, managing complex revenue streams and long-term debt obligations.

As public funding declined in many states and tuition increased, borrowing became a central mechanism for financing college. To understand how the United States reached more than $1.7 trillion in student loan debt, it is necessary to examine how financial aid developed and how the structure of higher education changed over time.

When College Was (Mostly) Free

Many early American colleges charged little or no tuition. Institutions such as Harvard University and the University of Virginia were funded largely through religious organizations, private donors, or state legislatures.

An example from higher prestige universities that did charge fees: Students at Brown University paid $75 per year (about $3,000 in modern U.S.D.)

The 1862 Morrill Act established land-grant universities across the country by allocating federal land to states to finance colleges focused on agriculture and mechanical arts. Because these institutions were publicly supported, tuition remained relatively low.

In this period, higher education was widely treated as a public investment designed to promote economic development and civic participation.

The Birth of Modern Federal Aid

The modern federal financial aid system began with the Servicemen's Readjustment Act (GI Bill) in 1944, which expanded access to college for returning veterans following World War II.

In 1965, President Lyndon B. Johnson signed the Higher Education Act, formalizing federal involvement in grants and student loans. The legislation aimed to broaden access to postsecondary education, particularly for lower- and middle-income students.

At this stage, loans were designed to supplement grants and family contributions. Over time, however, as tuition rose and grant funding did not keep pace, loans became a primary financing mechanism.

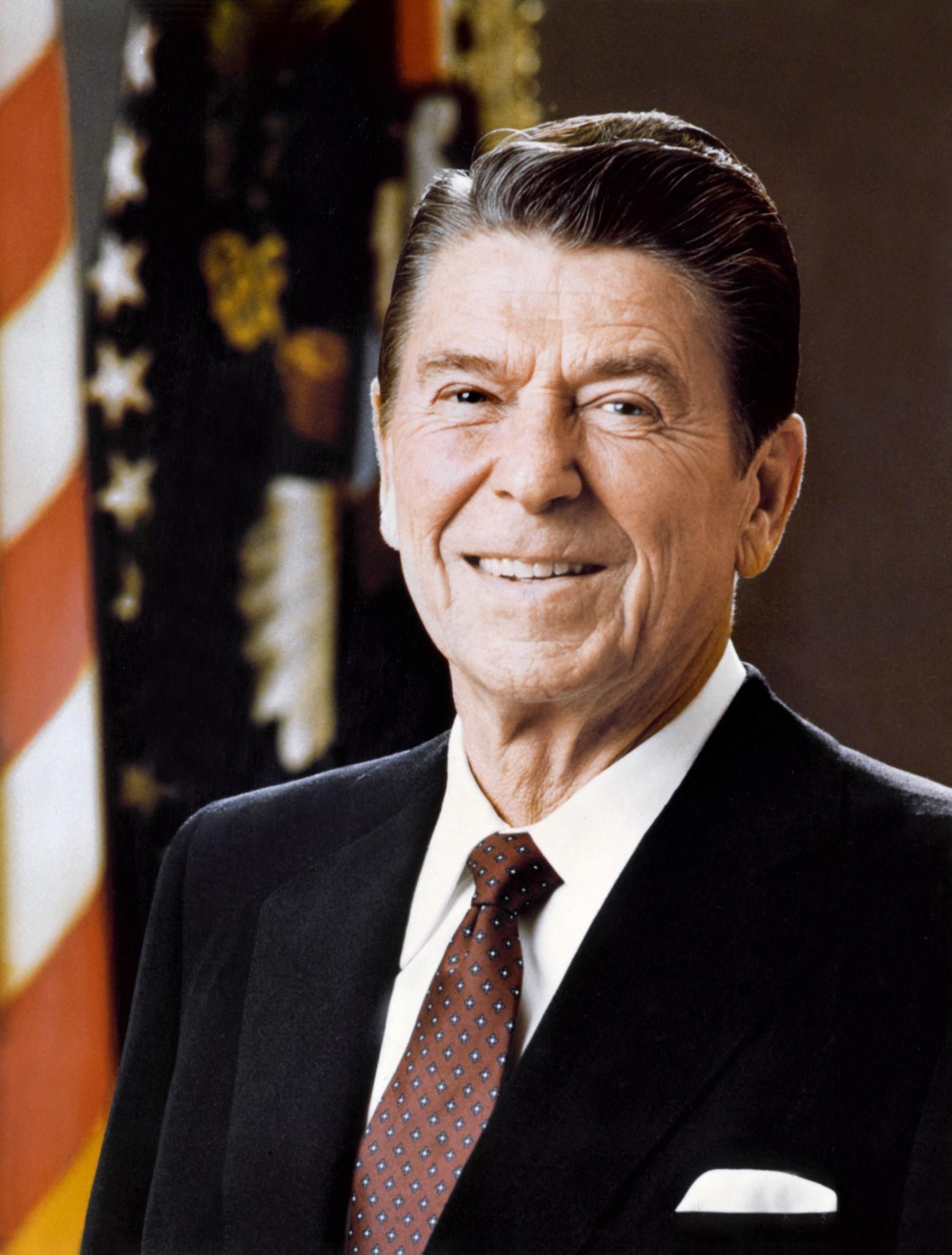

The Political Pivot: Reduced Public Subsidy

By the late 1960s and 1970s, public universities faced increased political and fiscal scrutiny. An adviser to then–California Governor Ronald Reagan stated:

“We are in danger of producing an educated proletariat. … That’s dynamite! We have to be selective on who we allow [to go to college].”

Whether interpreted as a budgetary concern or an ideological statement, the broader shift that followed was measurable: state appropriations per student declined in many regions, and tuition revenue grew in importance.

As public subsidy decreased, institutions relied more heavily on tuition. As tuition rose, borrowing increased.

The financial responsibility for higher education shifted progressively from the state to the individual student.

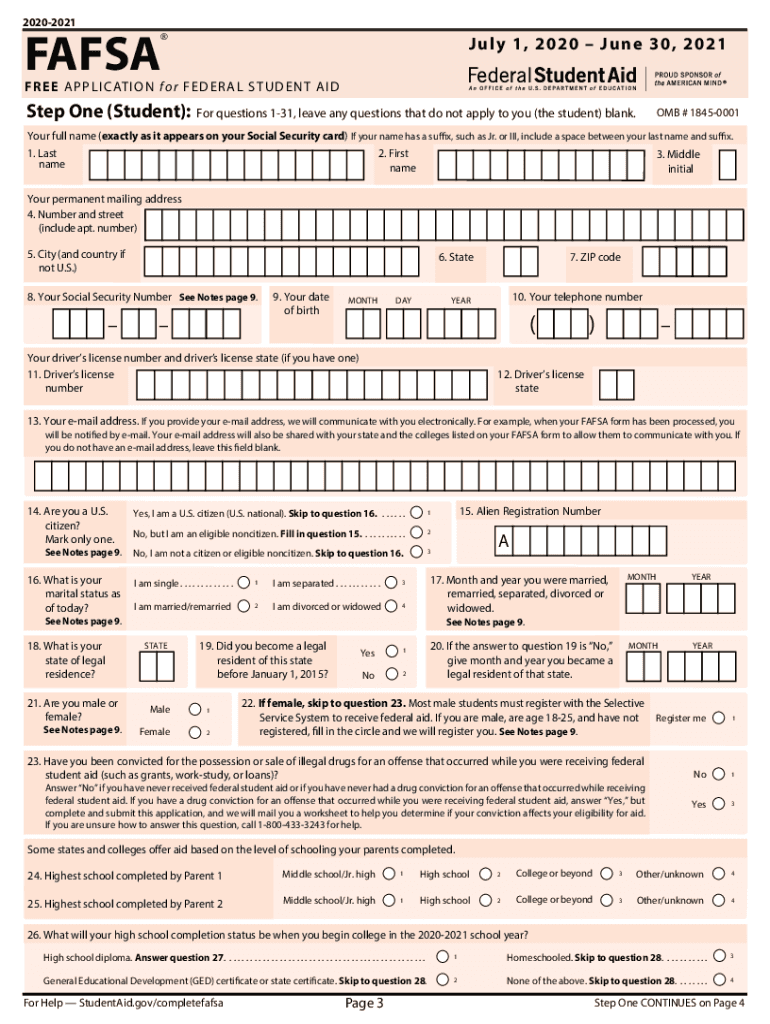

The FAFSA: Then and Now

The Free Application for Federal Student Aid (FAFSA) was designed to standardize access to federal aid programs.

Early versions were shorter and administratively simpler.

Today’s FAFSA, particularly following the FAFSA Simplification Act, functions within a highly regulated framework that includes:

- Required IRS Direct Data Exchange consent

- Multiple financial “contributors”

- Student Aid Index (SAI) calculations

- Federal database matches (SSA, NSLDS, DHS, VA)

- Verification and correction procedures

The governing structure is detailed in the U.S. Department of Education’s Federal Student Aid Handbook (Application & Verification Guide, 2025–2026). While the application interface has been modernized, the regulatory environment behind it has grown more technical.

Families now navigate:

- Federal grant formulas

- Loan limits and aggregate caps

- State eligibility rules

- Institutional aid methodologies (including CSS Profile requirements)

- Verification documentation standards

- Professional judgment policies

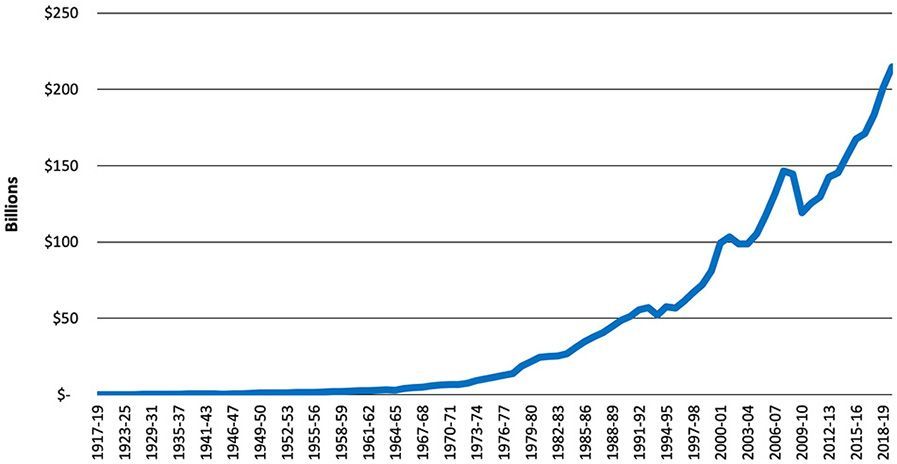

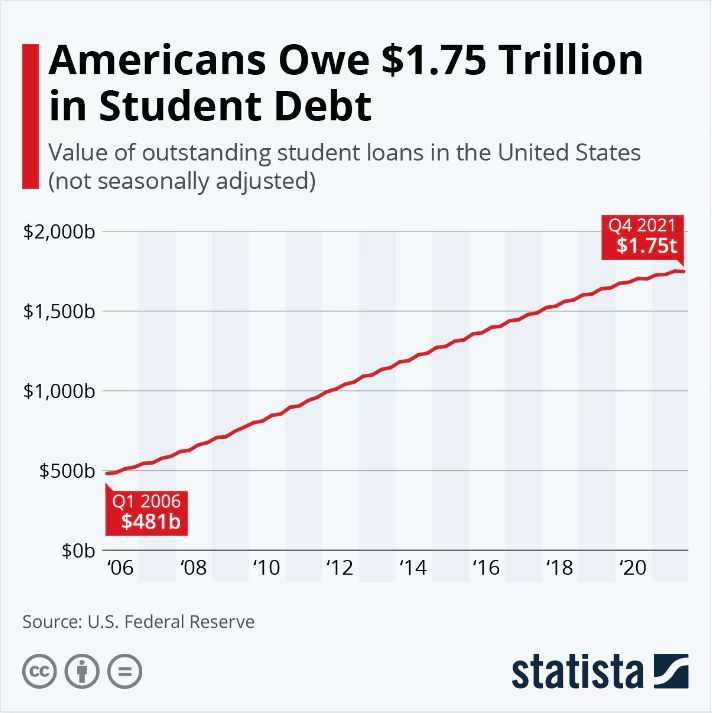

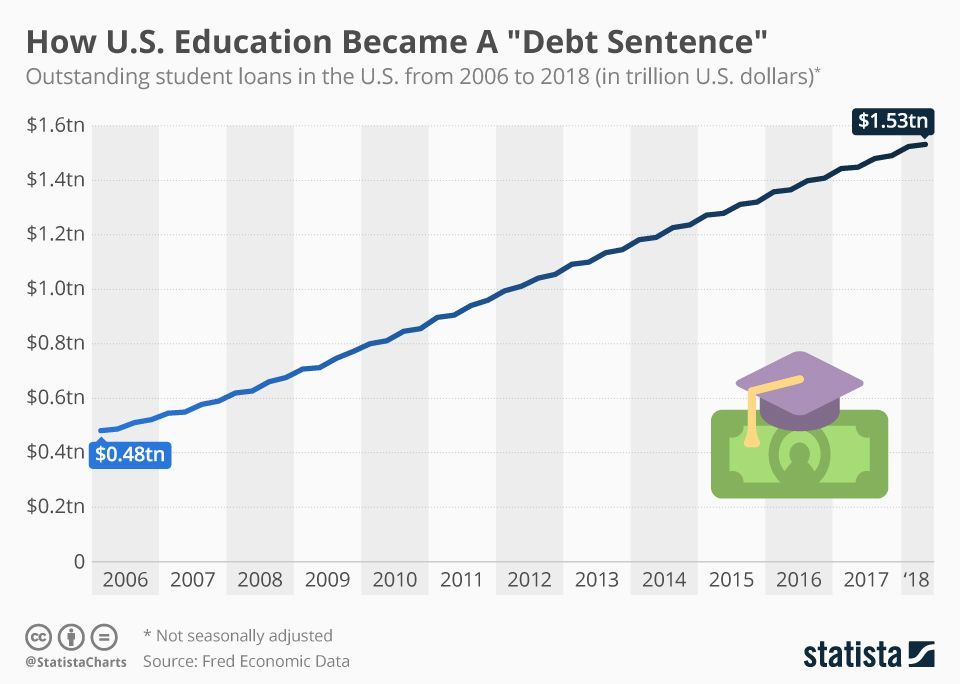

The Expansion of Student Debt

According to the Federal Reserve, outstanding student loan debt in the United States exceeds $1.7 trillion, distributed among more than 43 million borrowers.

College Board reports that inflation-adjusted tuition and fees have increased significantly since the 1980s, particularly at public four-year institutions as state funding per student declined.

The relationship between reduced public appropriations, rising tuition, and increased borrowing is well documented in higher education finance research.

Student loans have become a normalized component of financing postsecondary education.

Federal Reserve data portal: https://fred.stlouisfed.org/series/SLOAS

College Board Trends in College Pricing: https://research.collegeboard.org/trends/college-pricing

Financial Aid Advising and Growing Complexity

In previous decades, many families could reasonably interpret financial aid awards without specialized assistance.

Today, families must evaluate:

- The difference between SAI and actual net price

- Federal versus institutional eligibility

- Enrollment status impacts on aid

- Loan origination limits and cumulative caps

- Repayment plan structures

- Verification and correction requirements

We would predict that financial aid advising is likely to become a professional service that families use in the same way they use accountants, because the regulatory framework, documentation requirements, and financial consequences have become too complex for most individuals to manage confidently on their own without professional guidance.

Sources

- History.com – “American Colleges Were Once Tuition-Free”

- Bunk History – “The Origin of Student Debt: Reagan Adviser Warned Free College Would Create a ‘Dangerous Educated Proletariat’”

- AACRAO Connect – “The FAFSA: Then and Now”

- U.S. Department of Education – Federal Student Aid Handbook, 2025–2026 Application & Verification Guide

- Federal Reserve Bank of St. Louis (FRED) – Student Loan Debt Outstanding (SLOAS)

- College Board – Trends in College Pricing and Student Aid

You might also like

The Tuition Aid Journal